Global Investing for Indian Clients: Feeder Funds vs IBKR vs GIFT City (2026)

Indian investors have three routes to access global markets: domestic feeder funds, direct investing through foreign brokers, and GIFT City outbound mutual funds. Each route has a different tax structure, compliance burden, and investor profile. Here is a clear breakdown of all three.

Why Global Investing Belongs in Every Client Portfolio

Most clients picture global investing as a bet on US tech. It is better understood as risk management. A portfolio held only in India quietly carries four separate risks that a home bias hides.

The rupee erodes what clients already own. Over the past two decades the rupee has lost roughly 3 to 4 percent a year against the dollar, and the slide has accelerated. It crossed 90 for the first time in late 2025 and now trades near 95. A portfolio compounding at 12 percent in rupees, but losing 4 percent to currency, really delivers closer to 8 percent in hard-currency terms. A client holding only Indian assets is carrying a currency bet they never consciously placed.

Clients' future bills are partly priced in dollars. This is the other side of the same coin, and it is easy to miss. Much of everyday spending tracks imported, dollar-denominated inputs. Fuel is the clearest example: petrol and diesel move with global crude, so a weaker rupee feeds into transport, food, and manufacturing costs. Larger still are the dollar liabilities many families already plan for: a child's foreign education, overseas travel, an eventual relocation. Those are dollar bills with a due date, and rupee savings alone are an awkward way to fund them.

India is a small slice of global equity. Indian listed companies make up only about 3 to 4 percent of global market capitalisation. A portfolio built entirely at home leaves out the other 96 percent or so of investable equity by construction. Since asset allocation drives most long-term return and risk, that is a large, unintended single-country concentration, not a neutral default.

The biggest growth themes are not listed in India. The companies leading AI infrastructure, advanced semiconductors, and the clean-energy supply chain sit mostly in the US, Taiwan, South Korea, and Europe. India's sharp underperformance against global peers in 2025 was driven partly by its thin exposure to the AI theme that lifted markets elsewhere. Clients cannot buy what is not listed, and an India-only mandate rules these companies out.

None of this is an argument against India. Over long horizons Indian equities have held their own, even after currency. The point is narrower: global exposure works as a structural hedge and as a way to build hard-currency assets over time. For most clients the question is not whether to hold it, but how.

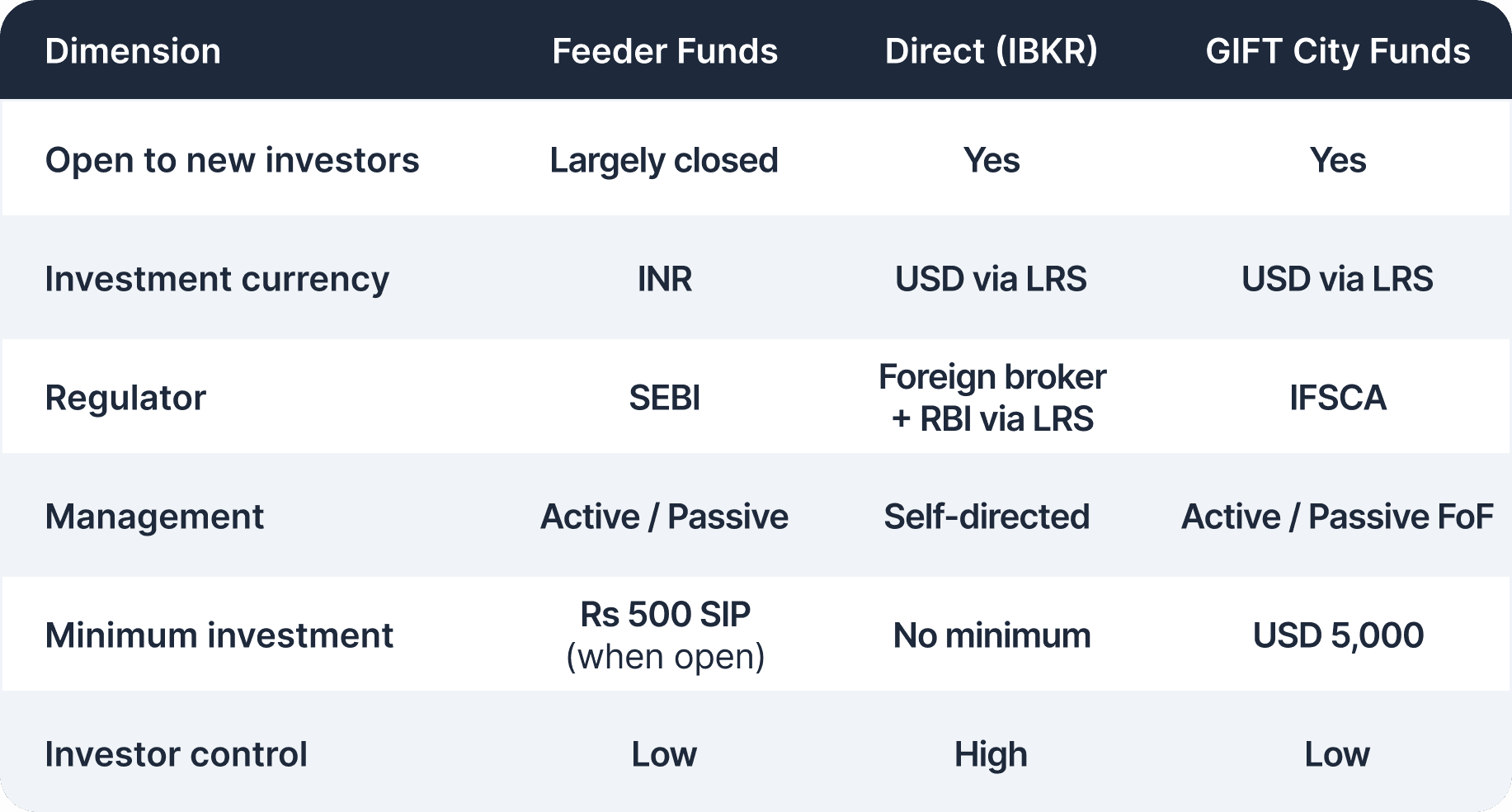

Three Routes to Global Investing

There are three ways clients can currently access global equity markets from India. Each operates differently at the structure, tax, and compliance level.

Feeder funds: Indian SEBI-regulated mutual funds that invest in overseas securities, transacted in INR

Direct investing via foreign brokers: Buying stocks or ETFs on foreign exchanges through a platform like Interactive Brokers, using the RBI's LRS framework

GIFT City outbound funds: Mutual funds domiciled in India's International Financial Services Centre, regulated by IFSCA, transacted in USD via LRS

Route 1: Feeder Funds

Feeder funds are SEBI-regulated mutual funds that pool client money in INR and route it into overseas markets, typically via a master fund domiciled abroad. Motilal Oswal S&P 500 Index Fund, ICICI Prudential US Bluechip Equity Fund, and Franklin India Feeder – Franklin U.S. Opportunities Fund were the standard instruments for global equity exposure through the early 2020s.

The RBI imposed a $7 billion aggregate cap on total overseas investment by the Indian mutual fund industry. That cap was exhausted by early 2022. Per SEBI's guidelines on overseas investment limits, most feeder funds have been closed to fresh SIPs and lump sum investments since then, with only occasional reopening windows.

International funds don't qualify as equity-oriented under Indian tax law, since they invest in foreign rather than domestic equity. Their tax treatment has changed twice in recent years, and the current position differs from what many older guides still show.

Under the Finance Act 2023, international funds were classed as "specified mutual funds" and taxed at the investor's slab rate regardless of holding period, with no LTCG benefit. The Finance (No. 2) Act 2024 then narrowed that definition with effect from FY 2025-26: a specified mutual fund is now one that invests more than 65% in debt and money-market instruments. International equity funds no longer meet that test, so they move back to the general capital gains grid. For redemptions in FY 2025-26 and FY 2026-27, the treatment is:

Held 24 months or less: short-term capital gains, taxed at the investor's slab rate

Held more than 24 months: long-term capital gains, taxed at 12.5% without indexation

The older slab-rate-regardless-of-holding-period rule still governed redemptions made before 1 April 2025, so positions sold in earlier years may have been taxed differently. The ₹1.25 lakh LTCG exemption is specific to equity-oriented schemes and may not extend to international funds, so confirm the exact figure with a CA.

This does not change the bottom line for new money: feeder funds are largely closed to fresh SIPs and lump sums since the industry's overseas investment cap was exhausted, with only occasional reopening windows. The constraint is access, not tax.

Route 2: Direct Investing via Foreign Brokers

The Liberalised Remittance Scheme (LRS) is the RBI framework governing all outward remittances by resident Indians — it applies to investing via foreign brokers and to GIFT City funds alike. Under LRS, each resident Indian can remit up to USD 250,000 per financial year for any permitted purpose, including investments, foreign education, medical treatment, travel, and maintenance of relatives abroad.

For the direct route, the client opens an account with a foreign broker, remits funds from an Indian bank via Form A2, and buys stocks or ETFs on foreign exchanges. Interactive Brokers is the most commonly used platform for this purpose.

US ETFs vs UCITS ETFs: a distinction that changes the risk profile

US-domiciled ETFs (SPY, VOO, VTI, QQQ) are US situs assets. Under US estate tax rules for non-resident aliens, an Indian investor holding more than USD 60,000 in these assets at death faces estate tax at 25 to 40 percent on the total. India has no bilateral estate tax treaty with the United States. This risk is real, frequently overlooked, and worth flagging to any client building a direct global portfolio.

UCITS ETFs, domiciled in Ireland or Luxembourg under the EU's UCITS regulatory framework, are not US situs assets. Estate tax does not apply. Accumulating UCITS share classes (which reinvest dividends rather than distributing them) also carry no dividend tax during the holding period. iShares Core S&P 500 UCITS ETF (CSPX.L) charges 0.07% annually in management fees, one of the lowest-cost ways to hold broad global equity exposure.

Currency taxation on the direct route

On the direct route, capital gains are computed in INR. If a client buys a stock at USD 100 when the exchange rate is Rs 83, then sells it at USD 100 when the rate has moved to Rs 90, there is a taxable gain of roughly Rs 700 per share in INR — even though the stock itself did not move in dollar terms. The rupee depreciation is embedded in the capital gain calculation and is taxable.

Compliance requirements

Schedule FA (the foreign assets disclosure schedule in the annual ITR) must be filed every year the client holds foreign assets, even at zero gain. The penalty under the Black Money Act for non-disclosure is Rs 10 lakh per assessment year. Clients also need to track USD cost basis, declare DTAA credits for US withholding tax on dividends, and convert gains to INR using the SBI TT rate on the purchase date.

Route 3: GIFT City Outbound Funds

GIFT City (Gujarat International Finance Tec-City) is India's International Financial Services Centre, located in Gandhinagar. Its funds are regulated by IFSCA under the Fund Management Regulations 2022. Under FEMA, GIFT IFSC entities are treated as persons resident outside India, placing them outside the RBI's $7 billion overseas MF cap entirely. This is why outbound funds continue launching through GIFT City while mainland feeder funds remain closed.

Resident Indians investing in GIFT City funds still use LRS to remit USD. The 20% TCS on amounts above Rs 10 lakh applies and is claimable at ITR filing.

For a complete breakdown of GIFT City's regulatory structure and product categories, see the Creso guide to GIFT City.

Active and passive structures

DSP Global Equity Fund (launched June 2025) is an actively managed fund selecting 30 to 50 large-cap stocks across the US, Europe, and Asia. The minimum investment is USD 5,000 (roughly Rs 4.5 lakh). The direct plan TER is 1%; the regular plan TER is 1.75%. There is a 1% exit load for redemptions within two years, aligned with the LTCG holding threshold.

Parag Parikh AMC's IFSC S&P 500 FoF and Nasdaq 100 FoF (NFO opened February 2026) are passive fund-of-fund structures investing 90 to 100% of the corpus into UCITS ETFs rather than holding US stocks directly. The direct plan TER is 0.30%; the regular plan TER is 0.60%. Because these funds hold UCITS ETFs at the underlying level, there is no US situs exposure at any layer.

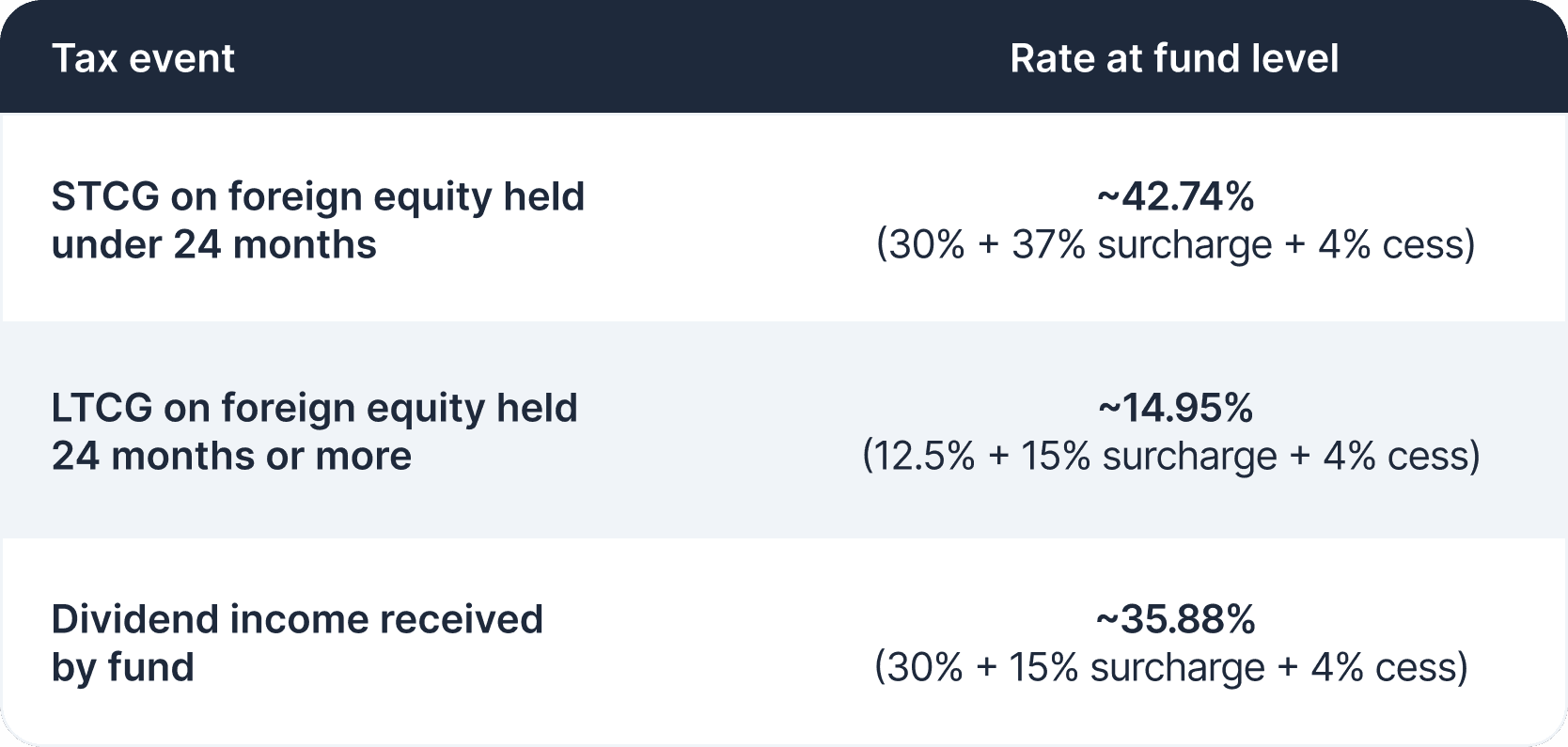

Fund-level taxation

GIFT City outbound funds pay tax on their own trading activity before declaring NAV. The investor does not pay a separate capital gains tax at redemption — the NAV already reflects the fund's post-tax position.

Funds that trade frequently within 24 months carry significant NAV drag from the 42.74% STCG rate. Funds holding positions for 24 months or more pay the much lower LTCG rate. This is why longer holding periods and exit loads are built into the fund design.

On estate tax for GIFT City fund investors

Even though DSP Global Equity Fund holds US-listed stocks directly, investors in the fund have no US estate tax exposure. Investors hold units of a GIFT City trust, which is India-domiciled. US estate tax applies to direct ownership of US situs assets, not to holding units of an Indian-domiciled fund that holds those assets internally. PPFAS FoFs go further, holding UCITS ETFs at the underlying level, creating an additional layer of separation from US situs assets.

Why GIFT City Works Well for Indian Investors

GIFT City outbound funds have structural and practical advantages that are worth understanding clearly before advising clients.

Funds run by names clients already trust. DSP, Edelweiss, and Parag Parikh AMC have established track records and are known entities in the Indian market. Clients are not being asked to trust an unfamiliar foreign platform with their savings.

No foreign brokerage account or manual forex management. The KYC process uses Aadhaar and PAN, subscriptions and redemptions work on familiar NAV-based mechanics, and the AMC handles all currency conversion internally. There is no need to track individual positions across foreign exchanges or maintain records of USD cost basis for every transaction.

No US estate tax exposure. Investors hold India-domiciled fund units, not US situs assets. The estate tax liability that accompanies direct investing in US-listed instruments simply does not arise. For say PPFAS FoFs, the UCITS ETF structure creates an additional buffer.

No tax on rupee depreciation gains. On the direct IBKR route, a weakening rupee creates a taxable INR gain even if the underlying asset has not moved. On GIFT City funds, clients invest and redeem in USD. Rupee depreciation during the holding period does not generate a taxable event at the investor level. The benefit of dollar appreciation accrues without triggering a separate capital gain. (Given the unsettled position on investor-level tax at GIFT City fund redemption, confirm the full treatment with a CA before advising clients.)

Indian regulatory coverage for global markets. IFSCA is an Indian regulator. Clients get access to global markets without stepping outside India's regulatory perimeter, which is meaningful comfort for investors cautious about foreign regulatory jurisdictions.

A distributor-led model with aligned incentives. Opening a foreign brokerage account on IBKR is cumbersome for most clients, while GIFT City funds onboard through a familiar distributor-led flow. The incentive structure also differs: a brokerage model earns per transaction, which quietly rewards churn, whereas the fund model earns on the asset management fee. The distributor is paid to keep clients invested and growing, not to generate turnover.

Where Creso Comes In

For distributors, the practical challenge with GIFT City is not understanding the products. It is managing them across multiple AMCs, each with separate onboarding flows, transaction portals, and client records.

Creso solves this. MFDs can onboard clients across all GIFT City AMC offerings in one place, process transactions digitally without navigating individual AMC portals, and give clients a single consolidated view of their full portfolio (Indian mutual funds, SIFs, and GIFT City holdings) all on one platform. For distributors building global investing as a service offering, this removes the operational overhead that otherwise makes it impractical to offer at scale.

Key Risks to Keep in Mind

Currency risk is not one-directional. If the rupee strengthens, USD-denominated assets lose value in INR terms even if the underlying holding is unchanged. The long-term trend is depreciation, but annual movements vary.

GIFT City's product range is still early. As of mid-2026, available funds are equity-focused and concentrated on US and global developed markets. Fixed income, commodities, and multi-asset global exposure require the direct route via UCITS ETFs.

Direct route compliance is a long-term commitment. Schedule FA is annual and non-negotiable. A CA with cross-border experience is effectively required to manage this route properly.

FAQs

Q: Why can't clients invest in the old international mutual funds anymore?

A: The RBI capped total overseas investment by Indian mutual funds at $7 billion. That cap was exhausted by 2022. Most SEBI-regulated international feeder funds have been closed to fresh investments since. GIFT City funds operate outside this cap because IFSCA entities are treated as offshore under FEMA.

Q: What is the difference between a GIFT City outbound fund and a feeder fund?

A: Feeder funds are SEBI-regulated, INR-denominated, and tax gains at the investor's slab rate for units bought after April 2023. GIFT City outbound funds are IFSCA-regulated, USD-denominated, and pay fund-level tax on trading activity before declaring NAV. The investor does not pay a separate capital gains tax at redemption. They are structurally different products.

Q: Does a GIFT City fund investor face US estate tax if the fund holds US stocks?

A: No. The investor holds units of an India-domiciled GIFT City trust, not US stocks directly. US estate tax applies to direct ownership of US situs assets. Since the fund intermediates ownership, the investor's exposure is to Indian fund units. Funds routing through UCITS ETFs at the underlying level have no US situs exposure at any layer.

Q: What is TCS on LRS remittances, and does it affect client returns?

A: When a resident Indian remits more than Rs 10 lakh under LRS in a financial year, the bank deducts 20% as Tax Collected at Source. This is advance tax credited against total tax liability at ITR filing, and any excess is refunded. It creates a short-term liquidity drag on the remitted amount worth planning around for larger allocations.

Q: Why should clients on IBKR choose UCITS ETFs over US-listed ETFs?

A: US-domiciled ETFs are US situs assets. A client holding more than USD 60,000 in them at death faces US estate tax at 25 to 40 percent, with no treaty protection since India and the US have no bilateral estate tax agreement. UCITS ETFs, domiciled in Ireland or Luxembourg, are not US situs assets and carry no estate tax exposure. Accumulating UCITS classes also carry no dividend tax during the holding period.

MFDs looking to offer clients structured, compliant access to global investments can explore Creso's distributor platform at creso.in.