GIFT City Explained: A Distributor's Guide for 2026

GIFT City has gone from a policy ambition to a name that now turns up in real investor conversations, especially among those exploring overseas exposure and global investing. The numbers track that shift: it climbed to 43rd in the Global Financial Centres Index released in October 2025, up from 52nd a year earlier, and crossed 1,000 registered entities by 2025. This guide explains what GIFT City is, who regulates it, how its tax structure works, the products it offers, and what it means for mutual fund distributors.

What is GIFT City?

GIFT City stands for Gujarat International Finance Tec-City. It is located in Gandhinagar, Gujarat, and was notified in 2015 as India's first International Financial Services Centre (IFSC). An IFSC is a designated zone within India that operates under a specialized regulatory structure built for international, cross-border financial transactions, conducted largely in foreign currency.

This makes GIFT City both a physical financial district and a regulatory jurisdiction. An entity set up inside the IFSC is treated, under FEMA, as a person resident outside India. A fund domiciled there is therefore offshore for regulatory purposes, even though it is physically in Gujarat and run by AMCs that Indian investors already know. That structure is what the rest of the system is built on.

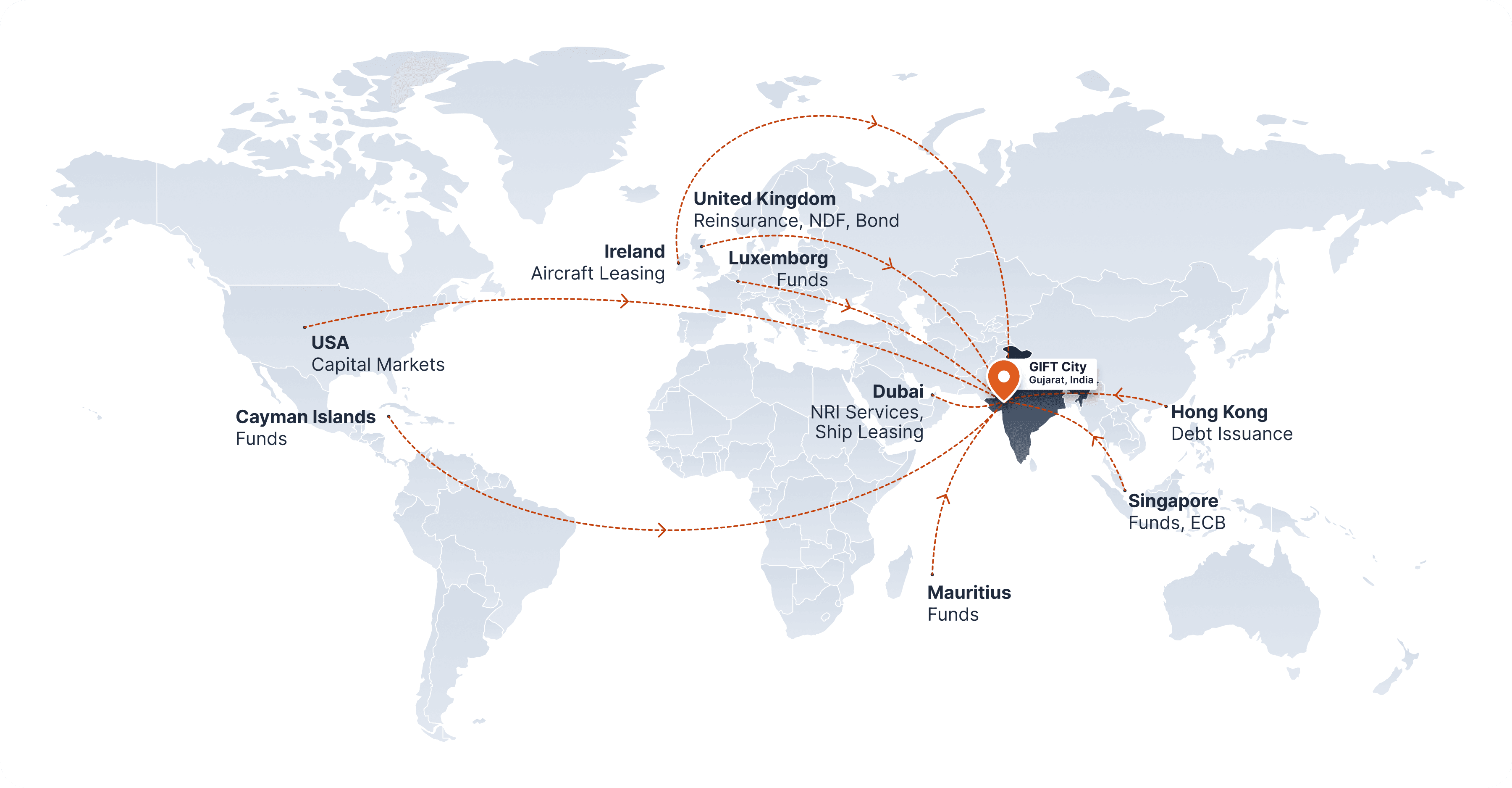

GIFT City is not a single product. It is a hub. Banking, fund management, insurance, aircraft leasing, a bullion exchange, two international stock exchanges, and a fintech sandbox all operate under the same roof and the same regulator.

A short history of GIFT City

GIFT City is a recent arrival in most investors' vocabulary, but the structure behind it has been building for close to two decades.

Year | Milestone |

2007 | The Percy Mistry Committee report recommends India build its own international financial center |

2011 | Foundation stone laid in January by then Finance Minister Pranab Mukherjee. |

2015 | India's first IFSC begins operations at GIFT City. At this stage it is overseen by the existing domestic regulators (RBI, SEBI, IRDAI) within their respective areas. |

2019 | Parliament passes the IFSCA Act, creating a dedicated regulator for the IFSC. |

2020 | The IFSCA began operations in October as a single unified regulator, taking over from the four domestic regulators within the IFSC. |

2022 | The India International Bullion Exchange (IIBX) launches in July, India's first bullion exchange. |

2025 | DSP launches India's first retail offshore fund from GIFT City. Tata launches the first retail inbound fund for NRIs. |

2026 | More AMCs launch funds and Budget 2026-27 doubles the unit tax holiday from 10 years to 20. |

The IFSC has existed since 2015, but the unified regulator that gives GIFT City its single rulebook is only about five years old. The pace of activity since then has been steep.

Why India built GIFT City

For decades, India suffered a massive leakage of financial business. Whether an Indian company was raising capital in dollars, a Non-Resident Indian (NRI) was investing global savings, or a fund manager was structuring an India-focused strategy, the transactions invariably flowed through offshore hubs like Singapore, Dubai, Mauritius, London, or Dublin. While the economic activity originated in India, the associated fees, jobs, and regulatory oversight were exported.

GIFT City was created to reverse this trend. It targeted the core strengths of offshore centers: Singapore's capital markets, Mauritius's investment structures, and Dublin's aircraft leasing and UCITS ecosystem; and recreated them within India through a dollar-denominated framework, a unified regulator, and competitive tax incentives. Aircraft leasing highlights the shift: by late 2025, GIFT City hosted 34 lessors managing 370 aviation assets, including 196 aircraft and helicopters, in a business once largely routed through Dublin and Singapore.

Beyond recapturing transactions, GIFT City aims to repatriate the entire financial value chain. A financial center is an ecosystem of specialized professionals—fund administrators, lawyers, accountants, tech teams, and compliance experts. When business went offshore, so did this lucrative cluster and the tax revenue it generated. By anchoring these operations domestically, India is building institutional capability and nurturing homegrown talent rather than renting it from other jurisdictions.

Ultimately, India's vision extends beyond domestic business. The country intends to evolve from a mere feeder market into a premier global financial and fintech hub, attracting international capital, institutions, and talent; even for transactions with no direct link to India. The establishment of international exchanges like India INX and NSE IFSC, alongside a new bullion exchange and expanding treasury operations, underscores this broader, global ambition.

The scale is no longer trivial. As of 2025, GIFT City IFSC hosts roughly 37 banks (20 of them foreign), total banking assets of about $100 billion, more than 200 fund management entities running over 340 funds, 50-plus insurance and reinsurance entities, and over 130 fintech firms. Operational funds have raised commitments of around $32 billion, of which roughly $14 billion has already been deployed into India. (reported via BusinessToday.)

Who regulates GIFT City: the IFSCA

Inside India, a financial firm answers to up to four separate regulators depending on what it does. The International Financial Services Centres Authority replaces all of them inside the IFSC, combining the functions that the RBI, SEBI, IRDAI, and PFRDA perform into one regulator with a single approval process.

Its remit is wide: banking, capital markets, insurance, pensions, fund management, leasing, and fintech all sit under it, with more on them in the next section.

A single regulator matters in practice for a few reasons: faster approvals, lighter compliance, and rules written to line up with global standards rather than retrofitted from domestic law. For a firm operating across both the mainland and the IFSC, the difference in turnaround time is real.

GIFT City offerings: the product map

GIFT City spans eight broad product categories. Only two come up often in mutual fund distribution, but the full map is worth knowing.

Category | What it includes | Relevant to MFDs? |

International Banking | Foreign currency savings accounts, foreign currency fixed deposits, trade finance, corporate treasury | Indirectly (NRI clients) |

Global Investment Products | Direct US investing, GIFT City mutual funds, AIFs | Yes, directly |

Insurance & Reinsurance | Cyber, marine, aviation, specialty commercial cover from global reinsurers | No |

Aircraft Leasing | Aircraft financing, leasing, aviation asset management | No |

Fintech Ecosystem | Sandbox testing for cross-border payments, wealthtech, insurtech, regtech | Watch this space |

Wealth Management | Global portfolios (US and European stocks, ETFs), family office structures, PMS | Yes, for HNIs and NRIs |

Bullion Exchange | Gold imports, bullion trading via IIBX | Niche |

Global Treasury Centres | Cash pooling, FX management, liquidity management | No |

Several of these categories are worth a brief note.

International banking is the entry point for NRIs: a dollar account on Indian soil(IFSC), with foreign currency deposits that sidestep the NRE and NRO maze.

Global investment products are the category most relevant to mutual fund distribution. This is where GIFT City mutual funds and AIFs sit, and where this guide keeps returning.

Insurance and reinsurance has pulled in more than 50 insurance and reinsurance entities writing specialized cover. Aircraft leasing is the standout success story, dragging business back from Dublin and Singapore. The fintech sandbox lets firms test cross-border payments and wealthtech without the full regulatory weight upfront. Wealth management serves UHNWIs and family offices building global portfolios. And the bullion exchange, IIBX, gives India a transparent, regulated marketplace for gold and silver imports, with SBI as its first trading-cum-clearing member.

Who is GIFT City actually for?

GIFT City serves a broad set of users, and the reason it works for each is different. It helps to be specific, because a client who hears "global financial hub" often assumes it is not for them.

Resident Indians. Anyone wanting dollar-denominated global exposure can use GIFT City outbound funds through the LRS.

NRIs. For non-residents, GIFT City is mostly a cleaner route back into India: USD bank deposits and USD-denominated funds that invest in Indian markets, with simpler repatriation than the usual NRE and NRO setup. Read more in the NRI's guide to GIFT City (coming soon).

HNIs and family offices. Global portfolios, succession planning, and wealth consolidation across jurisdictions, run from inside India's regulatory perimeter.

Corporates. Foreign currency borrowing, trade finance, and treasury operations managed onshore instead of in Singapore or Dubai.

Foreign Portfolio Investors (FPIs). ctment funds can establish India-focused FPIs in GIFT City rather than Singapore or Mauritius, keeping the fund structure, fees, and oversight onshore. SEBI also permits NRIs, OCIs, and resident Indians to hold larger stakes in IFSC-based FPIs than under the mainland regime

Startups and fintechs. The regulatory sandbox lets them test cross-border products without carrying the full compliance load from day one.

Global financial institutions. Banks, insurers, and asset managers wanting an India presence with offshore-style rules.

For mutual fund distributors, the opportunity concentrates in two of these groups: resident investors asking about global diversification, and NRIs looking to get exposure to the India growth story without the local tax and compliance hassles

Tax in GIFT City: what it truly means

The tax benefits in GIFT City are real but widely misread. The headline holidays apply to the units operating inside GIFT City, not to the person buying a fund. The main one is Section 80LA, under which an eligible unit can claim a 100% deduction on its business income for a block of consecutive years. The Finance Bill 2026 doubled that block from 10 years to 20, allowing the deduction for 20 consecutive years out of 25, effective 1 April 2026. After the holiday, income is taxed at a flat 15%, with a reduced 9% Minimum Alternate Tax and a 9% withholding rate on IFSC-listed bonds.

This architecture is what convinces a global bank or fund manager to set up shop. It is not a personal tax shelter. So what actually reaches the investor?

Tax feature | Who it benefits | What it means in practice |

80LA 100% deduction (20 of 25 yrs) | The unit (bank, fund manager, lessor) | Lowers the institution's cost of operating, not your client's tax bill |

Fund-level taxation on outbound funds | The structure | The NAV already reflects post-tax trading; no separate capital gains event for the resident investor at the fund level |

Capital gains exemption on certain securities | Non-resident investors | NRIs investing in qualifying GIFT City structures can be exempt from Indian capital gains tax |

No STT, CTT, stamp duty on IFSC trades | The investor | Lower transaction friction than mainland exchanges |

GST exemption on IFSC services | The investor | Services from IFSC units are outside GST for qualifying transactions |

Two cautions before acting on any of this. First, a resident investor still uses LRS to remit dollars, and 20% TCS applies on remittances above ₹10 lakh in a financial year (the threshold rose from ₹7 lakh on 1 April 2025). TCS is not a cost; it is advance tax that is claimed back at filing. But it is a cash-flow drag worth planning around. Second, two questions on outbound funds remain unsettled and are worth flagging to clients. Because a GIFT City fund is domiciled in India yet invested abroad through the LRS, it is unclear whether a resident must report it in Schedule FA, the foreign-asset section of the ITR; getting that wrong triggers Black Money Act penalties, so most CAs disclose to be safe. And because the fund is itself taxed on its gains, the same gain could be taxed again at the investor's redemption, with no clean credit to offset it. Confirm the exact position with a CA. The full comparison of how this stacks up against feeder funds and direct investing lives in our breakdown of global investing for Indian clients: feeder funds vs IBKR vs GIFT City.

What GIFT City means for MFDs

GIFT City hands you a product category that did not exist a few years ago: regulated, dollar-denominated global investing you can offer without sending clients off to a foreign platform you have no visibility into. For the first time, "I want US exposure" has an answer you can service and earn on, rather than losing the client to a direct app.

The opportunity splits cleanly into outbound and inbound.

Outbound is for your resident clients. They remit dollars under LRS and buy a GIFT City fund that invests abroad. The funds are real and live. DSP's Global Equity Fund launched in June 2025 as India's first retail offshore fund, a 30 to 50 stock global portfolio with a $5,000 minimum. Parag Parikh's IFSC S&P 500 and Nasdaq 100 funds-of-funds opened their NFO in February 2026, built on low-cost UCITS ETFs. Edelweiss runs a Greater China strategy. For the full, current list with minimums, expense ratios and more see which outbound GIFT City funds are live (coming soon).

Inbound is the NRI story, and it is where GIFT City removes the most pain. For NRI clients mainland onboarding seems too painful: rupee accounts, physical paperwork, KYC that stalls for weeks. GIFT City strips a lot of that out. The breakthrough came in September 2025, when Tata launched the first retail inbound fund, letting an NRI buy India exposure for as little as $500. The response has been steep. The retail investor base in GIFT City schemes rose about 177% in a single quarter, to roughly 3,438 by March 2026 from 1,239 in December 2025 (Outlook Money). The reach is also wider than most distributors assume, because inbound is not limited to NRIs. Any non-resident can invest, including a foreign national with no Indian connection at all, as long as they are from a FATF-compliant jurisdiction (currently excluding the US and Canada). And for many inbound structures a PAN is no longer required, since IFSCA's framework lets eligible non-residents invest without one where tax is handled at the fund level, which clears one of the biggest barriers that historically kept foreign money out of Indian schemes. For the live list, see which inbound GIFT City funds are live (coming soon).

Here is the catch. This is a different conversation than selling a domestic SIP. Clients will object. TCS will eat returns. IFSCA is too new. Why not just use Interactive Brokers. Having a structured answer to each one is what separates an MFD who sells this well from one who fumbles it. We built a full playbook on talking to clients about GIFT City and handling their objections(coming soon) for exactly that.

This also reflects a broader shift in distribution. The MFDs who add global and alternative products to a domestic book are the ones growing fastest, much like the operators who got serious about technology early. If you are still weighing whether modern distribution is worth the effort, our guide on how to become a mutual fund distributor in India covers the foundations.

And the operational reality: the friction with GIFT City is not understanding the products, it is managing them across multiple AMCs, each with its own onboarding flow and portal. That is the specific problem Creso's GIFT City tooling (coming soon) is built to solve, by letting you onboard and transact across GIFT City AMCs in one place and give clients a single consolidated view.

Common misconceptions about GIFT City

A handful of myths come up in almost every client conversation. Clearing them early saves you a lot of back-and-forth.

"GIFT City is tax-free." Partly, and it depends entirely on which side you are on. The 20-year tax holiday is for the units operating there, not for your client's returns, so for outbound funds your resident client's gains are still taxable. But for inbound funds, the picture flips: a non-resident investor is generally exempt from Indian capital gains tax under Section 10(4D), with no TDS at redemption. So "inbound is tax-free at the investor level" is fair to say, while pitching GIFT City as a blanket personal tax shelter for everyone is overselling it.

"It's only for the ultra-rich." Not anymore. Outbound funds start around $5,000 and the first retail inbound fund starts at $500. The minimums have fallen sharply over the last two years, and as more AMCs launch retail schemes the expectation is they fall further still in the coming months.

"It's too new to be safe." The regulator is young, but it is a statutory Indian authority with defined rules and disclosures. New is not the same as unregulated. And you are not handing money to an unknown: the funds are run by the same AMCs (DSP, Parag Parikh, Edelweiss, Sundaram) that have managed Indian investors' money for decades. That said, market-linked products still carry market risk, and that is worth saying plainly.

"It's the same as the old international feeder funds." No. Feeder funds are SEBI-regulated, rupee-denominated, and capped by the RBI's $7 billion industry limit, which is why they have been largely closed to fresh money since 2022. GIFT City funds are IFSCA-regulated, dollar-denominated, and sit outside that cap entirely.

"NRIs can't use it because it's on Indian soil." They can, and it is often easier than the mainland route. The offshore treatment under FEMA is exactly what makes repatriation cleaner for them.

FAQs

Q: What is GIFT City in simple terms?

A: GIFT City is the Gujarat International Finance Tec-City near Gandhinagar, home to India's first International Financial Services Centre. It is a zone inside India that operates under its own regulator and deals largely in foreign currency, so for most rules it is treated as offshore.

Q: Who regulates GIFT City?

A: The International Financial Services Centres Authority (IFSCA), set up under an Act of Parliament passed in 2019 and operational since October 2020. It is a single unified regulator that performs, within the IFSC, the functions the RBI, SEBI, IRDAI, and PFRDA handle on the mainland.

Q: Can resident Indians invest through GIFT City?

A: Yes. Resident Indians can invest in GIFT City outbound funds using the Liberalised Remittance Scheme, up to $250,000 per financial year. A 20% TCS applies on remittances above ₹10 lakh in a year, claimable at the time of filing returns.

Q: How is GIFT City different from the old international feeder funds?

A: Feeder funds are SEBI-regulated, rupee-denominated, and capped by the RBI's $7 billion overseas investment limit, which is why most closed to fresh money in 2022. GIFT City funds are IFSCA-regulated, dollar-denominated, and treated as offshore under FEMA, so they sit outside that cap.

Q: What can NRIs do in GIFT City?

A: NRIs can hold dollar deposits, invest in dollar-denominated India-focused inbound funds, and repatriate proceeds in foreign currency with no friction than the traditional NRE and NRO route. The first retail inbound fund launched in September 2025 with a minimum of around $500.

Q: Can a foreign national with no Indian connection invest in GIFT City?

A: Yes. GIFT City inbound funds are open to any non-resident from a FATF-compliant jurisdiction (currently excluding the US and Canada), not only NRIs or people with Indian ancestry. For many inbound structures a PAN is not required, because IFSCA's framework lets eligible non-residents invest without one where tax is handled at the fund level. This is a large part of why GIFT City is positioned as a genuine global gateway, not just an NRI product.

Q: Is GIFT City safe?

A: It operates under the IFSCA, a statutory Indian regulator, with defined rules and disclosures. The regulatory framework is sound, but market-linked products inside the zone still carry normal market risk like any other fund.

If you want to offer clients structured, compliant access to GIFT City without juggling a separate portal for every AMC, take a look at what Creso offers for MFDs.