An NRI's Guide to GIFT City for 2026

GIFT City funds are USD-denominated investment schemes based in India's International Financial Services Centre (IFSC) that let a non-resident Indian invest into Indian markets in foreign currency, without the compliance load of Indian mutual funds. The appeal lies in the fact that the gains carry no capital gains tax in India, nothing is deducted at source, and the proceeds stay fully repatriable. This guide explains what these funds are, how they compare with the other routes into India, who qualifies, how the money moves, and where the risks lie.

What is GIFT City and the IFSC?

GIFT City is India's first International Financial Services Centre, a financial zone in Gandhinagar, Gujarat, overseen by a single regulator, the International Financial Services Centres Authority (IFSCA). Businesses inside it operate in foreign currency, mostly US dollars, and qualifying investments get tax treatment the Indian mainland does not extend. Creso's GIFT City primer covers the zone in full; this article concentrates on how GIFT is relevant to NRIs.

Why inbound GIFT City funds suit an NRI

Inbound funds bring foreign money into Indian assets, and for a non-resident they solve four problems the mainland route cannot:

Your money stays in dollars the whole way through. The investor funds the investment in foreign currency and takes the capital and gains back out in foreign currency, fully repatriable. Nothing is converted into rupees at either end, so no foreign-exchange spread quietly eats into the investment on the way in or the way out.

The gains carry no Indian tax. There is no capital gains tax in India and nothing deducted at source, against the 12.5% to 30% that comes off a mainland redemption before the money reaches the investor. Fund fees are GST-exempt too, which trims the running cost.

There is far less Indian paperwork. There is no need to open an NRE or NRO bank account: the mainland route requires one, whereas an inbound GIFT fund can be funded straight from a foreign or IFSC account. And because these holdings attract no Indian tax, there is no Indian return to file for them, removing a recurring compliance chore.

What you owe is decided at home, not in GIFT City. What you owe is decided at home, not in GIFT City. Because India’s IFSC levies no tax on these gains, there's nothing here for a tax treaty to relieve. Whether you pay anything depends solely on your country of residence and its own rules. Capital and gains are fully repatriable in foreign currency.

For example: an NRI in Dubai who puts $10,000 in an inbound GIFT equity fund pays no TDS, converts nothing into rupees, files no Indian return, and repatriates the full proceeds on exit. The same $10,000 in a mainland equity fund can also end up free of Indian capital gains tax, because the India–UAE treaty lets a UAE resident be taxed only at home, where there's no capital gains tax. But that money still needs an NRE or NRO account, TDS is deducted when you sell, and getting it back means a UAE tax residency certificate, Form 10F, and an Indian tax return. Same zero-tax outcome for a Dubai NRI, far more paperwork.

The India mainland route still wins in places, mainly on breadth. GIFT City is new, so its shelf is narrow; the mainland offers a far wider range of fund strategies, and a rupee SIP built on rupee cost averaging fits it naturally. Inbound is a strong option, not a wholesale replacement.

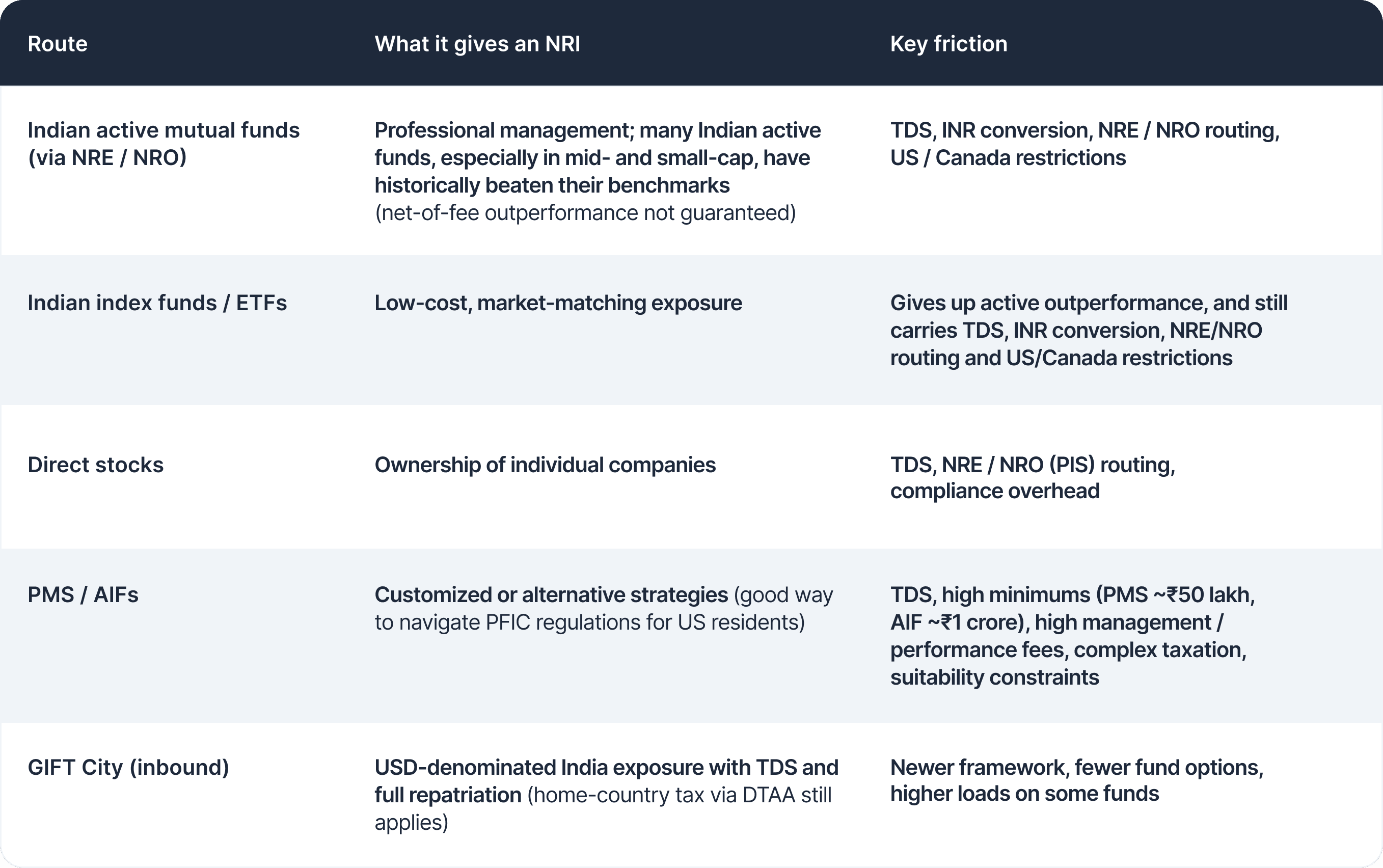

How inbound GIFT City funds compare with the other equity routes into India

For an NRI seeking equity exposure to India, here is how GIFT City stacks up against the other ways in. Each route does one thing well and charges a friction for it.

Every equity route involves a trade-off. Inbound GIFT City funds earn their place on tax and currency, not breadth of choice, which is still catching up. Retail funds such as the Tata India Dynamic Equity Fund and Sundaram's India Mid Cap GIFT already open from around $500 and $5000; a separate Creso guide compares the live funds.

A note on inbound versus outbound

GIFT City can be used in two directions. Inbound funds bring foreign money into Indian assets. Outbound funds send money from India into global markets such as US equities and ETFs. The direction decides which benefits apply, and for most NRIs, outbound adds little. Two reasons:

The same US and global funds are usually cheaper and far wider through the NRI's own resident channel: a US brokerage, a UK stocks-and-shares ISA (with its £20,000 tax-free annual allowance), or a Gulf platform. Routing that money back through India only adds a layer of cost.

Outbound funds are built for residents, not NRIs. Their draw is a lighter-taxed, still-open route into global markets, reached through the LRS: the RBI window that lets a resident send up to $250,000 abroad a year to invest. Neither half applies to an NRI. India doesn't tax their foreign gains in the first place, and LRS is resident-only, with their money already sitting offshore. So there's no tax to make efficient and no window to open.

Inbound is the opposite story: it brings offshore dollars into Indian markets with no India tax, no rupee conversion, and full repatriation. That is where the structure pays off for an NRI.

Myth vs reality

A few assumptions about GIFT City are worth dismantling, because each one stops NRIs who would actually qualify.

The first is that these funds are only for the wealthy. Retail inbound funds now start at roughly $ 500.

The second is that the paperwork is as heavy as the mainland's, and that you need an Indian bank account to take part. Neither holds. A PAN is not mandatory, the fund can be paid from a foreign or IFSC account, and onboarding is done remotely from abroad.

The third is that the money gets stuck in India. It doesn't: capital and gains are fully repatriable in foreign currency.

One thing that isn't really a myth: US and Canada NRIs face real limits. The current retail inbound funds, including Tata India Dynamic Equity and Sundaram India Mid Cap GIFT, exclude US and Canada residents for FATCA reasons. GIFT City's framework is more open than the mainland's in principle, and some institutional structures accept these investors subject to FATCA and CRS declarations. But retail access isn't there yet, and US persons carry PFIC reporting on top. A US or Canada NRI should confirm eligibility with the fund house rather than assume it.

Who's eligible, and how the money moves

Eligibility extends to NRIs, OCIs, and RNORs. The dividing line is the residency test: an individual who spends fewer than 182 days in India in a financial year is generally treated as non-resident for that year, the status these funds are built around. Resident Indians are explicitly excluded.

How the money is funded matters more than most NRIs expect. Inbound funds are bought in foreign currency, so the cleanest route is to remit dollars from a foreign or GIFT City (IFSC) bank account; an NRE account can also be linked. Using money straight from an NRO account is treated as round-tripping and is accepted by only a few fund houses (Aditya Birla Sun Life among them), and then only with Form 15CA and 15CB clearance; most AMCs take NRE or IFSC bank funding only. An NRI can also deploy India-sourced income such as rent or dividends, but NRO-to-NRE transfers are capped at USD 1 million a financial year under FEMA, which is worth planning around.

How an NRI actually invests

The established onboarding route is document-based rather than instant, but it works entirely from abroad. An investor completes the NRI KYC form and submits attested copies of a passport or tax ID plus proof of address, certified by a bank official, the Indian embassy, or a notary. Those documents go to the fund's registrar and transfer agent (an RTA such as CAMS, KFin, etc.) in GIFT City; once verified, the AMC opens a zero-balance folio, shares remittance details, and the investor funds it in dollars.

This is set to get lighter. Through a circular dated 31 October 2025, IFSCA extended video-based KYC (V-CIP) to low-risk NRIs in eleven specified jurisdictions, including the US, UK, Canada, UAE and Singapore. The process uses Aadhaar verification via DigiLocker and a live video call with anti-deepfake checks, with a foreign bank statement as proof of address (accounts open in debit-freeze until that first credit is verified). For now this is a regulatory framework still being rolled out, and fund houses are not yet onboarding investors through it.

Beyond funds: USD savings and deposits

Inbound GIFT City exposure is not limited to funds. IFSC Banking Units of major Indian banks now offer USD-denominated savings accounts and deposits, paying up to about 4.75% as of late 2025 (worth re-checking against current rates), against well under 2% at most US banks. The interest is tax-free in India for NRIs, with no TDS, and the same account can fund an inbound GIFT fund directly.

Risks and honest caveats

The upside is real, and so are the trade-offs. The IFSCA framework is younger than mainland regulation, with fewer investor precedents. Cost is the most underrated risk: a fund with a 3% entry load and a high expense ratio can erase a meaningful slice of the tax advantage, so the benefit has to be read net of fees. Currency runs both ways too, since dollar denomination suits an NRI who earns in dollars, but a stronger rupee lowers the return in rupee terms.

The USD savings and deposits described above carry a separate caveat: held in IFSC Banking Units, they sit outside DICGC deposit insurance, the cover that protects domestic bank deposits up to ₹5 lakh. With the fund universe still small, an inbound GIFT City fund works best as one component of a wider plan, not a replacement for a whole portfolio.

Building inbound GIFT City funds into a wealth plan

The core proposition is simple: inbound GIFT City funds give an NRI tax-efficient, USD-denominated access to Indian markets, with no TDS and full repatriation. The sensible next steps are to review the current India allocation, confirm the investor's country and residency status qualify, compare funds on cost rather than tax alone, and speak to a GIFT-empanelled adviser or AMC before moving money. The shelf is widening through 2026, and those who understand the structure early stand to benefit most.

FAQs

Q: Are inbound GIFT City fund gains taxable in India for an NRI?

A: No. Capital gains from inbound GIFT City funds carry no capital gains tax in India for a non-resident, and no TDS is deducted at source. Fund fees are also exempt from GST.

Q: Can US and Canada NRIs invest in GIFT City funds?

A: In many cases, yes. Unlike mainland Indian mutual funds, which widely restrict US and Canada investors, GIFT City funds are generally more open to them, subject to a FATCA and CRS declaration. Eligibility still varies by fund and some opt out, so confirm with the fund house, and US persons should account for their own PFIC reporting obligations.

Q: Do NRIs need an NRE or NRO account, or a PAN, to invest?

A:No. Inbound funds are paid in foreign currency from a foreign or GIFT City (IFSC) account, so no NRE or NRO account is needed. A PAN isn't mandatory either.

Q: What is the minimum investment, and do the funds charge loads?

A: Minimums and costs vary widely. The Tata India Dynamic Equity Fund opens at USD 500 with no entry or exit load and a total expense ratio capped at 1.75% for direct plans, while Sundaram's India Mid Cap GIFT carries a higher minimum and an entry load on some plans. Compare a fund on cost as well, not just on its tax benefit.

Q: Is money invested in inbound GIFT City funds fully repatriable?

A: Yes. Funds are fully repatriable in foreign currency.

Advisers building an NRI-focused practice can run the mainland side of the book on a modern platform and add the IFSC empanelment on top. See what Creso offers for MFDs.