GIFT City Outbound Retail Funds (2026)

GIFT City retail funds are USD-denominated global schemes run from India's IFSC and regulated by the IFSCA, letting resident Indians invest abroad from as little as USD 5,000. As of July 2026, five such funds are live across four AMCs: two passive index funds, two active global funds, and one regional fund.

This guide covers what each fund holds, what it costs, what the exit rules are, so you can determine who it fits and place clients without digging through five separate factsheets.

What "GIFT City retail funds" actually means

Retail schemes are USD-denominated funds set up under the IFSCA (Fund Management) Regulations, 2025, housed in India's IFSC at GIFT City. Residents buy them by remitting dollars under the LRS. Because the fund is treated as offshore, it sits outside the RBI's overseas mutual fund cap, which is why new funds keep launching here while domestic feeder funds stay shut.

The plumbing behind all of this, the regulator, tax holidays, LRS, TCS and onboarding, is covered in GIFT City explained: a distributor's guide, and how this route stacks up against feeder funds and direct broking is in feeder funds vs IBKR vs GIFT City. This piece assumes that background and stays on the funds themselves.

One point to set straight before the fund details: the GIFT City schemes are new, with the oldest investing only since September 2025, so none has a long track record as a fund. However, the AMCs running them are well established and are bringing existing strategies into a USD wrapper. The scheme's own history is too short to rely on even where the manager and mandate behind it are proven, so be clear about which track record is being quoted.

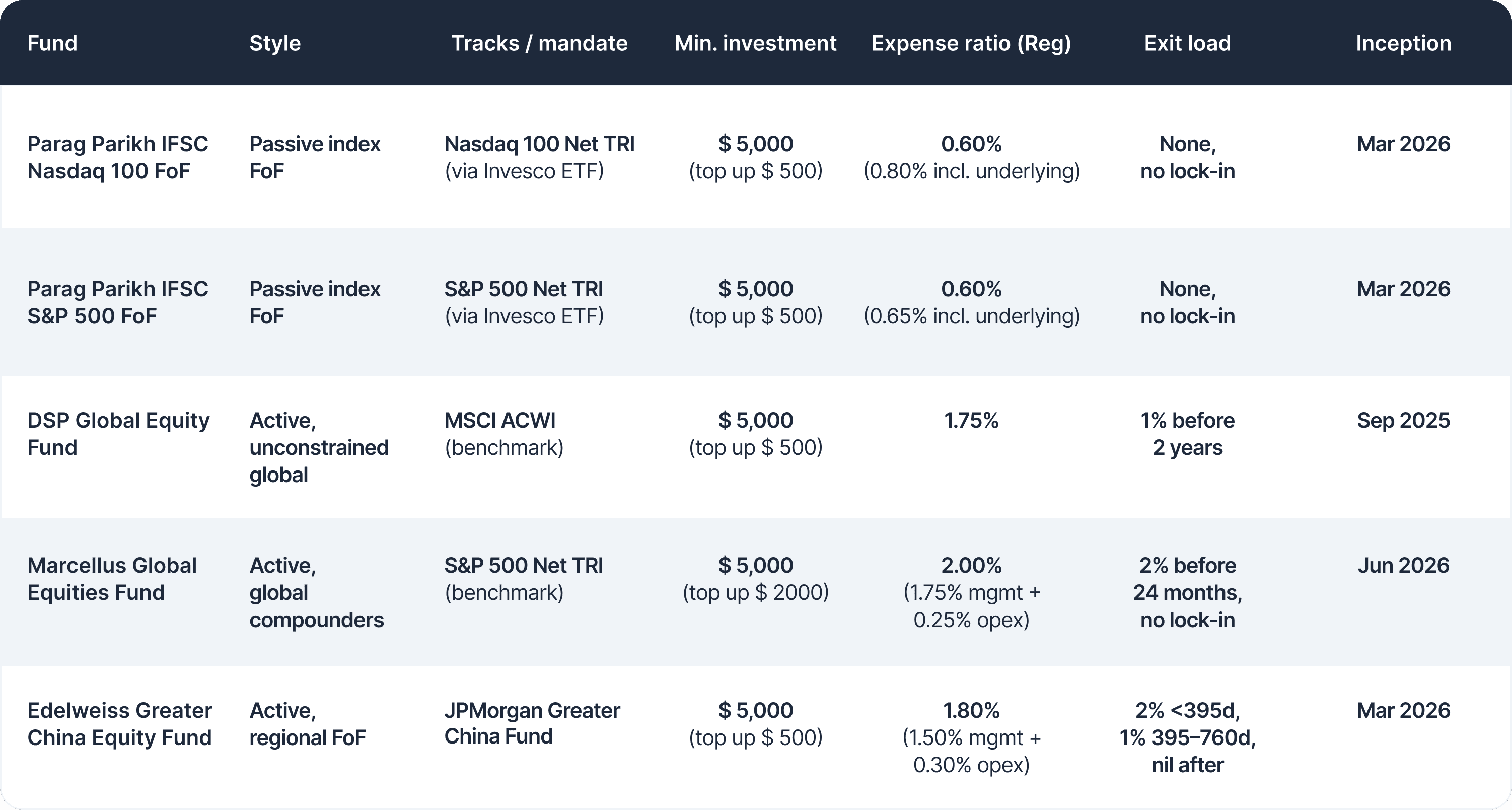

Funds at a glance

Passive index funds

These two do one job: track a US index at low cost. Both come from PPFAS Alternate Asset Managers IFSC, the GIFT City arm of the house behind Parag Parikh Flexi Cap. Both are fund-of-funds that hold a single underlying Invesco UCITS ETF, both carry no entry or exit load, and both have no lock-in. That makes them the cleanest "core global allocation" building blocks on this list.

Parag Parikh IFSC Nasdaq 100 Fund of Fund

What it holds. The fund puts almost all of its money, 99.96%, into a single instrument: the Invesco NASDAQ-100 Swap UCITS ETF, which mirrors the Nasdaq 100 Net Total Return Index, with the small remainder held in cash. That gives a client exposure to the 100 largest non-financial companies listed on the Nasdaq, and the index leans heavily toward technology. As of March 2026, information technology made up just over half the basket at 50.2%, followed by communication services at 15.3% and consumer discretionary at 12.6%.

Structure and managers. This is an open-ended passive fund-of-fund, registered as a retail scheme with the IFSCA. Rather than buying US shares directly, it feeds into a Europe-listed UCITS ETF, which keeps the structure simple and avoids holding US-situs assets at the investor level. It is benchmarked to the Nasdaq 100 Notional Net Total Return Index and managed by Akshay Falgunia, with Nirmal Bari serving as Director and Principal Officer. The full portfolio and sector breakdown are set out in the fund's factsheet on PPFAS's GIFT City site.

Costs and exit. The scheme charges 0.60% a year, which rises to about 0.80% once the fee of the underlying Invesco ETF is included. A client can start with USD 5,000 and add money in steps of USD 500. There is no entry or exit load and no lock-in, so the investment can be redeemed at any time.

Performance so far. As a passive fund, what matters is tracking, not last month's number: expect the Nasdaq 100's return minus the roughly 0.80% all-in cost. One quirk to know: because the underlying ETF trades in Europe, the month-end NAV can show a gap of around 0.80% versus the US index simply because European markets close before New York, and it reverses the next trading day. So a month-end gap is usually noise, not underperformance. The factsheet carries the live number.

Distributor take. This is the cleanest and cheapest way on the list to give a client concentrated US technology growth in dollars. It suits an investor who specifically wants the Nasdaq's growth tilt and understands that the same concentration driving the returns also makes it more volatile than a broad-market fund.

Parag Parikh IFSC S&P 500 Fund of Fund

What it holds. Like its Nasdaq sibling, this fund holds a single underlying ETF, the Invesco S&P 500 UCITS ETF, at 99.90% of assets with the rest in cash, and that ETF tracks the S&P 500 Net Total Return Index. The result is far more diversified than the Nasdaq fund because it spans 500 of the largest US companies. As of March 2026 the sector mix ran to information technology at about a third (32.3%), then financials (12.5%), communication services (10.5%), consumer discretionary (10.0%) and healthcare (9.8%). The holdings and sector split are laid out in the fund's factsheet on PPFAS's GIFT City site.

Structure and managers. It is an open-ended passive fund-of-fund, registered as an IFSCA retail scheme and benchmarked to the S&P 500 Net Total Return Index. It uses the same feeder-into-a-UCITS-ETF structure as the Nasdaq fund and is run by the same team, Akshay Falgunia with Nirmal Bari as Director and Principal Officer.

Costs and exit. The scheme fee is 0.60% a year, and the all-in cost including the underlying ETF is about 0.65%, marginally cheaper than the Nasdaq fund because the S&P 500 ETF itself costs less to run. The minimum is USD 5,000 with additional purchases from USD 500, and there is no load and no lock-in.

Performance so far. As a passive fund, it should mirror the S&P 500's return minus its roughly 0.65% all-in cost. Like the Nasdaq fund, its month-end NAV can show a small gap versus the US index because the underlying ETF trades in Europe and closes earlier, a difference that unwinds the next session. Judge it on tracking accuracy over time, not any single month. The factsheet has the latest figures.

Distributor take. This is the natural default for a first-time global investor. Because it spreads across 500 companies instead of leaning into technology, it is an easier conversation and a lower-drama holding than the Nasdaq fund, while still capturing the long-run growth of the US market.

Active global funds

Here a manager builds a portfolio rather than tracking an index. Higher fees, higher potential for both out- and under-performance, and a philosophy the client is really buying into.

DSP Global Equity Fund

What it holds. This is a concentrated, actively managed global portfolio that held just 27 companies as of April 2026, spread across the US, Europe, Taiwan, the UK, Singapore and a set of Chinese businesses. What stands out is how little it resembles its benchmark. Where the MSCI ACWI Index carries roughly 65% in the US, this fund held under 30% there, and it was sitting on an unusually high 27.1% cash position. The manager is explicit that the cash is a by-product of valuation discipline rather than a market-timing call, and that the fund will stay on the sidelines when it cannot find ideas that clear its return hurdle. Its ten largest holdings, close to 43% of the book, included Amazon at 7.2%, alongside Adyen, TSMC, Meta, Tencent and Alphabet, and the team expects to eventually own 30 to 40 stocks. The thinking behind the portfolio is set out each month in the fund's factsheet and newsletter on DSP's GIFT City site.

Structure and managers. It is an open-ended active retail fund registered with the IFSCA, run by DSP Fund Managers IFSC and benchmarked to the MSCI ACWI Index. The stated approach is long-only, bottom-up and valuation-conscious, with a recommended holding period of 3 to 5 years, so it is designed for patient money rather than short holding periods.

Costs and exit. The Regular plan charges 1.75% a year and the Direct plan 1.00%, with no performance fee. Clients start at USD 5,000 in USD 500 increments, and there is a 1% exit load if they redeem within two years.

Performance so far. Because the portfolio looks nothing like the index, expect its returns to diverge from the MSCI ACWI, sometimes sharply, in either direction. It trailed early on by avoiding the expensive AI-hardware names driving the index, which flows from its valuation-first process rather than signalling a problem. Wide divergence is the design, not a defect, so judge it over a full 3-to-5-year cycle. The factsheet and monthly newsletter carry the current numbers.

Distributor take. This one is for a patient, valuation-aware client who wants a portfolio that looks nothing like the index and is willing to be early. It is the wrong fund for anyone chasing recent performance, and setting that expectation upfront is the difference between a client who stays the course and one who redeems at the first lull

Marcellus Global Equities Fund

What it holds. Marcellus builds a high-conviction portfolio of global "compounders" around four long-term themes it expects to absorb trillions of dollars of spending over the coming decade. The first is defence and aerospace, where annual capex now runs above a trillion dollars and suppliers such as GE Aerospace hold order books stretching out ten years. The second is power generation, where global electricity demand has stepped up to about 4% a year since the arrival of generative AI, implying roughly 400 GW of new capacity and around USD 600 billion of capex annually. The third is the AI build-out itself, where spending on chip foundries and data centres runs near USD 600 billion a year and flows to companies like TSMC. The fourth is luxury, where brands such as Hermes hold pricing power over a billionaire class growing about 7% a year. Representative holdings named by the AMC include Airbus, GE Aerospace, Amphenol, TSMC, LVMH and Hermes. Find more details on the Marcellus Global Equities Fund page.

Structure and managers. Unlike the passive PPFAS funds, this is a directly managed global equity portfolio, and Marcellus runs it with real US presence: its American arm, Marcellus International Investment Managers LLC, is registered with the US SEC as an investment adviser. The strategy is led by Arindam Mandal, the New York-based Head of Global Equities who previously ran global equities at Principal Global Investors, supported by Jaibir Sethi (Head of Global Research, formerly head of public-markets research at Premji Invest), Prashant Mittal (Fund Manager and CFA charterholder covering the global consumer sector) and Kalpesh Soni (Principal Officer at GIFT City with more than 20 years in capital markets). The fund is offered to Indian residents and Indian corporations.

Costs and exit. The Regular plan carries a total expense ratio of 2% a year, made up of a 1.75% management fee and 0.25% of operating costs, which makes it the most expensive fund on this list. The minimum is USD 5,000 with top-ups of USD 2,000, and there is a 2% exit load before 24 months with no lock-in.

Performance so far. There is no track record for this scheme yet, and getting this right with clients matters most. The returns in Marcellus's materials belong to its Global Compounders PMS, a separate product running since October 2022, not to this fund. That PMS has a strong long-run record in dollars, but it is a different vehicle, so presenting its numbers as this fund's would be misleading. Sell the strategy and the team, and be explicit that the PMS record is context, not a promise.

Distributor take. This is the priciest option here, aimed at clients who want an actively managed, thematic global portfolio and who trust the Marcellus name and process. With no fund history to point to, the case has to be built on the philosophy, the four megatrends, and the strength of the on-ground US team.

Active regional funds

A regional fund concentrates on one geography. Higher single-market risk, but useful for a client who wants a specific bet rather than broad exposure.

Edelweiss Greater China Equity Fund

What it holds. This is a fund-of-funds that channels money into the JPMorgan Funds Greater China Fund, an actively managed portfolio investing in growth companies across mainland China, Taiwan and Hong Kong. It is worth being clear that the active management comes from that underlying JPMorgan fund, which blends bottom-up company research with a top-down macro view, rather than from Edelweiss selecting stocks itself. By country, the book was roughly 51% mainland China, 45% Taiwan and 3% Hong Kong as of April 2026, and it is heavily tilted to technology, with information technology at about 47% of the portfolio and consumer discretionary next at around 17%. Its largest positions were TSMC at 9.34%, Tencent at 7.81% and Alibaba at 6.19%. The full holdings and country mix are in the fund's factsheet on Edelweiss's GIFT City site.

Structure and managers. It is an open-ended fund-of-fund under the IFSCA retail framework, run by Edelweiss Asset Management (IFSC Branch) with Ajitkumar Paudel as fund manager. Because it invests through JPMorgan's fund, the client is effectively buying JPMorgan's Greater China research capability delivered inside an Indian GIFT City wrapper.

Costs and exit. The fee has three layers a distributor should add up and explain. There is a management fee of 1.50% on the Regular plan (0.50% on Direct), operating expenses of up to 0.30%, and the underlying JPMorgan fund's own 0.62%, which is already reflected in the NAV. So the true all-in cost sits well above the headline 1.50%. The minimum is USD 5,000 with additional purchases from USD 500. The exit load depends on when the money went in: for investments made on or after 1 May 2026 it is 2% within 395 days, 1% between 395 and 760 days, and nil after 760 days.

Performance so far. Since the fund feeds into JPMorgan's Greater China fund, its return closely follows that portfolio minus the layered fees, so it lives or dies on Greater China equities and JPMorgan's stock selection. The scheme is only months old, so treat any since-inception figure as an early data point, not a trend. The factsheet has the current NAV.

Distributor take. This is a satellite holding rather than a core one. It fits a client who specifically wants exposure to China and Taiwan and can live with the concentration and geopolitical risk that come with a single-region bet. Both the layered fee stack and the tiered exit load need to be spelled out clearly before the client commits .

How to choose between them

Start with active versus passive. If the client just wants low-cost global exposure and no manager risk, the PPFAS S&P 500 or Nasdaq fund does the job at 0.60% to 0.80% all-in. If they want a manager to make active calls and will judge that over years, DSP, Marcellus or Edelweiss fit, at 1.5% to 2%-plus.

Then geography. The S&P 500 fund is the broadest single-country bet, the Nasdaq fund is a tech-tilted version of the same, DSP and Marcellus are whole-world, and Edelweiss is a focused Greater China play. Match breadth to how much concentration the client can tolerate.

Then cost and exit friction. Costs on this list run from 0.60% to over 2%, and exit loads range from none (both PPFAS funds) to 2% for up to two years (Marcellus, and Edelweiss on newer money). For a client who may need liquidity, the no-load passive funds are the friendliest.

Then currency. Every fund here is a rupee-depreciation hedge as much as an equity bet. Returns land in dollars, so a weakening rupee adds to rupee outcomes and a strengthening rupee subtracts. Clients treat the dollar exposure as free upside, so make sure they understand they are taking currency risk in both directions.

Tax works the same way across all five and is covered in full in the two articles linked above. In short: the fund pays tax at its own level, so the investor skips the annual foreign-asset reporting that direct US investing forces on them; long-term gains beyond two years are taxed at 12.5%; and remitting dollars draws 20% TCS above ₹10 lakh a year, reclaimable at filing. The two-year exit loads on most of these funds are set to line up with that long-term threshold, so factor holding period into the recommendation.

On the platform side, once a client is investing across GIFT City and domestic schemes, keeping the reporting in one place gets hard fast. Platforms like Creso, NJ Wealth and Prudent Corporate are where distributors consolidate that view.

FAQs

Q: What are GIFT City retail funds?

A: They are USD-denominated pooled investment schemes set up in India's IFSC at GIFT City and regulated by the IFSCA under the Fund Management Regulations, 2025. They let resident Indians and eligible investors access global markets from a minimum of USD 5,000, with the fund handling foreign taxes at its own level.

Q: How many GIFT City retail funds are live right now?

A: As of July 2026, five are live across four AMCs: PPFAS Nasdaq 100 and S&P 500 Fund-of-Funds, DSP Global Equity Fund, Marcellus Global Equities Fund, and Edelweiss Greater China Equity Fund. More are expected as additional AMCs launch schemes.

Q: How does a resident Indian invest in these funds?

A: Through the RBI's Liberalised Remittance Scheme, up to USD 250,000 per financial year. Onboarding is digital with PAN and Aadhaar, and no separate GIFT City bank account is needed. Remittances above ₹10 lakh a year attract 20% TCS, which is reclaimable when filing your ITR.

Q: Are GIFT City retail funds better than domestic international mutual funds?

A: They serve different needs. GIFT City funds are USD-denominated, count against the LRS limit, and settle tax at the fund level. Domestic international funds are rupee-denominated and simpler to buy, but many have faced inflow restrictions tied to overseas investment limits. GIFT City funds sidestep that constraint.

Q: What is the minimum investment in GIFT City retail funds?

A: USD 5,000 for all five current funds. Additional investments are typically USD 500, except Marcellus, which uses a USD 2,000 top-up.

Q: Which GIFT City fund has the lowest cost?

A: The two PPFAS passive funds. The S&P 500 FoF is 0.65% all-in and the Nasdaq 100 FoF is 0.80% all-in, versus 1.5% to over 2% for the active funds.

Q: Do these funds have a lock-in?

A: None of them have a lock-in. Both PPFAS funds have no exit load either. DSP charges 1% before two years, Marcellus 2% before 24 months, and Edelweiss uses a tiered load that falls to nil after 760 days on newer investments.

If you want to place these funds without stitching together five factsheets and separate reporting for GIFT City and domestic holdings, see how Creso helps MFDs run a modern practice.